The Central Board of Indirect Taxes and Customs (CBIC) has extended the facility of deferred payment of Customs import duty to a new category called Eligible Manufacturer Importers (EMI). This facility allows eligible importers to obtain Customs clearance first and pay the assessed import duty later, within prescribed due dates. For manufacturers, this improves liquidity and reduces working capital blockage while keeping shipments moving through ports, airports, and ICDs.

Brief on the scheme:

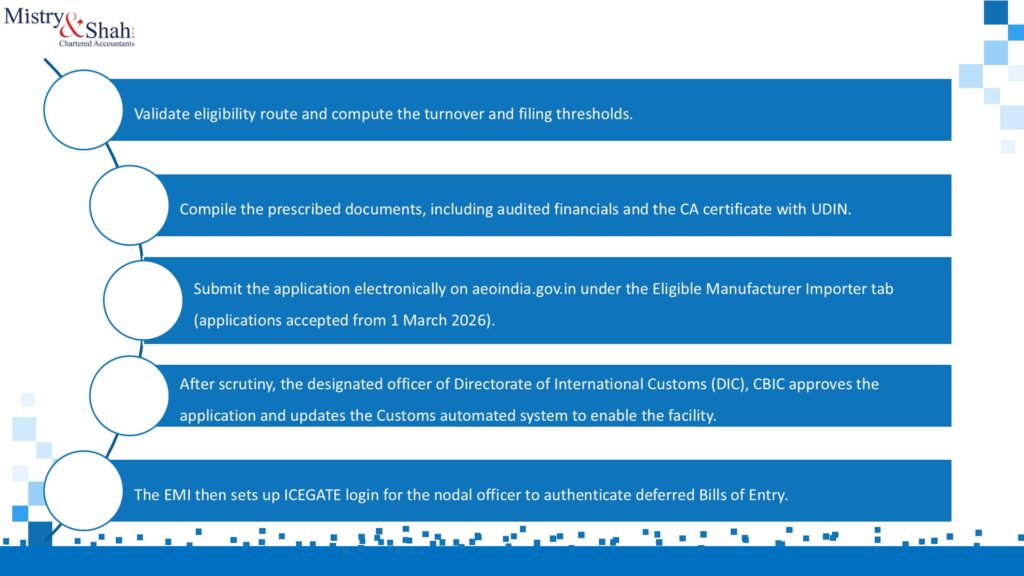

- Applications can be submitted online from 1 March 2026 on the AEO India portal (aeoindia.gov.in) under the EMI tab.

- The facility becomes available to approved EMIs from 1 April 2026.

- For Bills of Entry returned for payment during any month other than March, duty is payable by the 1st day of the following month. For March imports, duty is payable by 31 March.

- A nodal officer must authenticate deferred Bills of Entry on ICEGATE using OTP. Clearance is provided only after authentication.

- Strong compliance is essential. Delays can trigger interest liability and may lead to withdrawal of the facility or suspension/revocation of EMI approval.

What is deferred payment of import duty?

Deferred payment is a trade facilitation mechanism that delinks duty payment from Customs clearance. In simple terms, it follows the principle: clear first, pay later. Once enabled for an

eligible importer, goods can be cleared after required authentication, and the duty can be paid on or before the due date for the deferred period.

Who can use the EMI facility?

An applicant can qualify through one of the following routes:

Route A: Manufacturer Importer

- The applicant is an importer and a manufacturer, and has at least one active GSTIN where the nature of business activity is declared as factory or manufacturing in GST REG-01.

- The relevant GST registration is at least two financial years old as on the application date.

Route B: Importer using job work (Section 143 of CGST Act)

- If the applicant is not a manufacturer, it can still qualify if it sends inputs or capital goods to a job worker for job work under Section 143 of the CGST Act.

- The relevant GSTIN should have filed the last two half-yearly ITC-04 returns.

- The job worker must have an active GSTIN and declare factory or manufacturing in GST REG-01.

Note: MSME applicants have a relaxed minimum requirement for EXIM filings. Existing AEO-T1 entities that meet the EMI eligibility conditions can also apply.

Key eligibility conditions:

CBIC has prescribed detailed conditions. The most practical conditions for self-check are below:

| Area | What CBIC expects |

| Importer credentials | Valid IEC issued by DGFT and importer status under the Customs Act. |

| Customs footprint | At least 25 EXIM documents filed in the previous financial year (relaxed to 10 for MSMEs). |

| GST registrations | At least one active GST registration under CGST/SGST. |

| Manufacturing declaration / job work | Manufacturer must declare factory/manufacturing in REG-01, or job work route requires ITC-04 and job worker manufacturing declaration. |

| Turnover threshold | Aggregate turnover across all GSTINs under the same PAN exceeds Rs. 5 crore in the last financial year. |

| Business continuity | Business activities for at least two financial years preceding the application. |

| GST compliance | All pending GSTR-3B returns filed as on application date. |

| No tax collected but not deposited | No instances under GST, and no legacy excise/service tax collected but not deposited. |

| Financial solvency | CA certificate in prescribed format (with UDIN) and audited financial statements for last two years. |

| Legal integrity | No arrests, convictions, or pending prosecutions under relevant laws; not insolvent, in liquidation, or bankrupt. |

How to apply (step-by-step)

How it works after approval (operations)

- While filing the Bill of Entry, select payment method as ‘D’ (Deferred) in the payment method column.

- The nodal officer logs into ICEGATE and authenticates the deferred Bills of Entry using OTP sent to the registered email or mobile. Multiple Bills of Entry can be authenticated in one go.

- After authentication, Customs clearance is granted for the consignment under the Deferred Payment of Import Duty Rules.

- The importer pays the duty for the deferred period on or before the due date. Payment can also be made earlier if desired.

Due dates for duty payment

| Bills of Entry returned for payment | Duty payment due date |

| 1st day to last day of any month other than March | 1st day of the following month |

| 1st day to 31st day of March | 31st March |

Controls, defaults, and risk management

Deferred payment is a facilitation measure. It works best when importers maintain disciplined controls for authentication and payment. If duty is not paid by the due date, interest becomes payable. Repeated defaults can lead to loss of the deferred payment facility and a shift back to transaction-wise duty payment. For EMIs, CBIC may also suspend or revoke EMI approval if the importer becomes ineligible or non-compliant.

- Assign clear ownership: a nodal officer for ICEGATE authentication and a finance owner for duty payment.

- Implement a daily tracker of Bills of Entry filed with payment flag D and their deferred challans.

- Maintain a payment calendar and pay ahead of time during month-end congestion.

- Review GST compliance status and ensure no pending GSTR-3B returns at the time of application and thereafter.

- Audit access to ICEGATE OTP channels (email and mobile) and maintain segregation of duties.

Common questions (quick answers)

Q: Is the facility automatic after approval?

A: Yes. Once approved, CBIC updates the Customs automated system to enable the facility for the importer.

Q: Can duty be paid before the due date?

A: Yes. The importer can pay deferred challans at any time before the due date.

Q: Does the facility apply to every Bill of Entry?

A: Only when the Bill of Entry is filed with payment method flag D and authenticated by the nodal officer.

Q: What is the most common reason for delays?

A: Incomplete documents, mismatch in GST declarations, pending returns, and solvency documentation gaps.

How we can help

Mistry and Shah Global Services Private Limited can support you end-to-end:

- Eligibility assessment and gap closure plan

- Document collation, verification, and submission readiness pack

- Application filing support and response during scrutiny

- ICEGATE nodal officer setup and OTP control design

- Post-approval compliance monitoring and due-date alerts

Documents referenced:

- CBIC Circular No. 08/2026-Customs, dated 28 February 2026.

- Customs Notification No. 12/2026-Customs (N.T.), dated 1 February 2026.

- Deferred Payment of Import Duty Rules, 2016 (as amended).

- AEO India portal and ICEGATE guidance for deferred duty payment authentication.

Disclaimer:

This article is intended solely for informational and knowledge-sharing purposes. The contents are based on publicly available information, including notifications, circulars, and rules issued by the CBIC. While reasonable care has been taken in preparing this material, the information should not be construed as professional advice or a legal opinion.

Readers are advised to evaluate the applicability of the provisions to their specific facts and circumstances and seek professional advice before taking any action based on this article. Mistry & Shah Chartered Accountants shall not be responsible for any loss or consequence arising from reliance on this material.