The question of “where to register” under GST has never been a mere procedural formality, it has been a recurring issue of litigation, even under the erstwhile tax regime, for a simple reason, registration determines the State’s share of revenue. Consequently, it continues to remain an area of close departmental scrutiny and professional debate.

Under the GST framework, registration is fundamentally linked to the place from where the supply is made. This principle often becomes complex when goods are stored or dispatched from warehouses, cold storages, or third-party facilities.

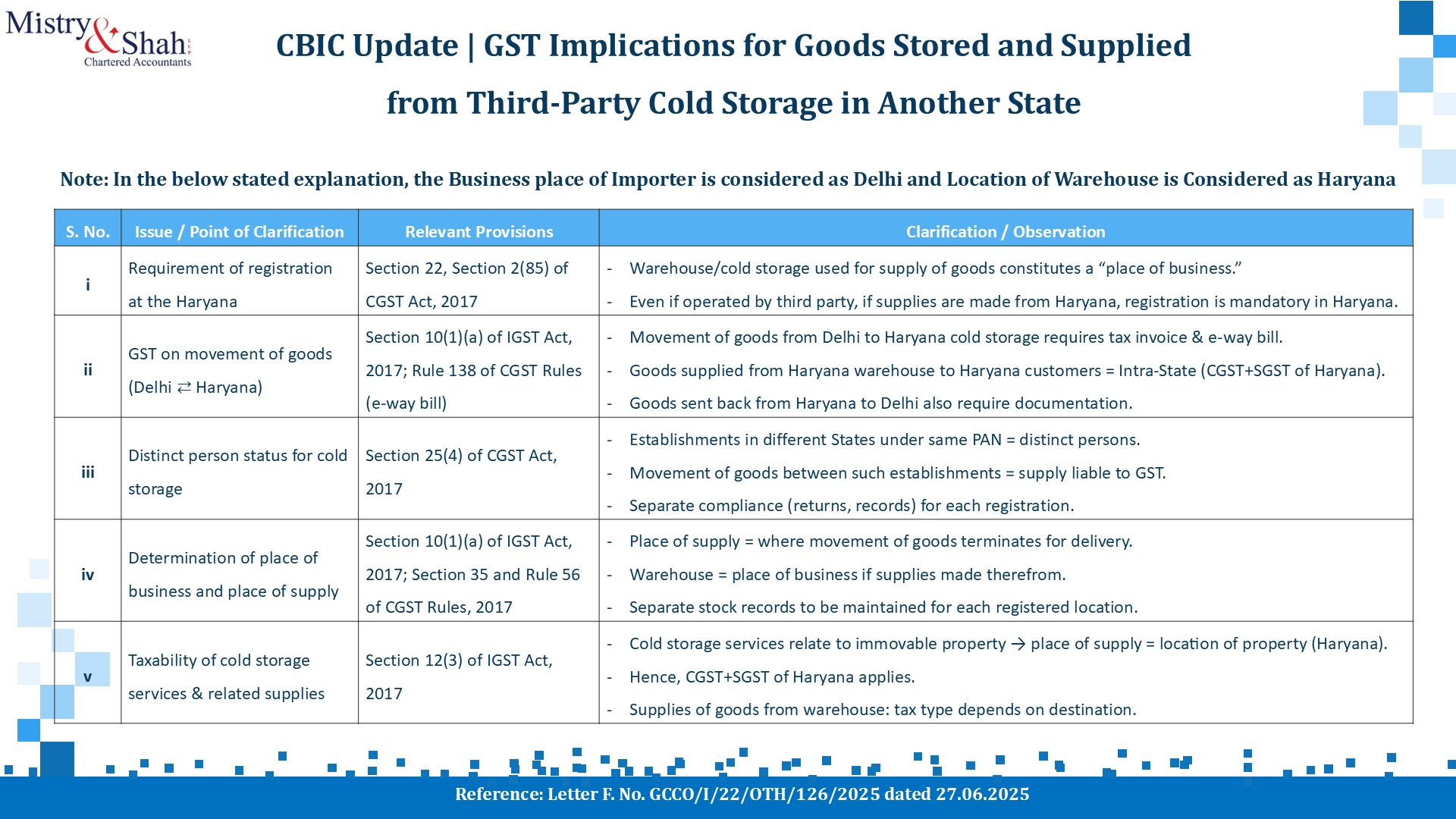

CBIC Clarification Rekindles the Debate

A recent communication issued by the Central Board of Indirect Taxes and Customs (CBIC), vide File No. CBIC-20016/75/2025-GST/1025 dated 25.09.2025, addressed to the Delhi Commissionerate, has brought this topic back into focus.

The communication reiterates that where goods are imported and stored in a cold storage or warehouse in the importing State, the storage premises must be separately registered under GST.

Further, all compliances, including invoicing, tax payment, and return filing must be undertaken from that registration.

Additionally, any movement of goods between the principal registered place and such storage premises would be treated as a supply between distinct persons, requiring a tax invoice and payment of GST.

While this clarification reinforces a settled principle, it raises practical questions on the scope and applicability of registration requirements for temporary or incidental storage facilities. A detailed explanation gathered from circular is produced in image below:

The Practical Dilemma, Is Every Storage a “Place of Business”?

The real question is:

Can officers insist on separate GST registration for every storage location used temporarily or occasionally during movement of goods?

Let’s consider a few common situations encountered by businesses:

-

Imported goods temporarily stored at a customs bonded or private warehouse near the port until transportation is arranged or the final buyer’s location is confirmed.

-

Short-term storage resulting from vehicle breakdowns or unforeseen logistical delays.

-

Temporary storage during change of vehicle in long-distance movement.

-

Goods retained at supplier’s location in bill-to–ship-to transactions, where dispatch occurs from the supplier’s premises, but the commercial intent and ownership lie with the buyer/importer.

In these cases, though goods may physically move from a storage point, the economic intent of supply originates from the buyer or importer. The GST law, however, does not define “temporary movement”, leaving substantial room for interpretation.

Interpreting the True Intent of Supply

It is possible for an assessee to argue that the intent and initiation of supply arise from the registered unit, even if dispatch occurs from another location. The decisive factor should therefore be intent of use and continuity of activity, rather than the mere existence of storage.

-

Where the storage is used occasionally or temporarily for logistical reasons, without any independent supply or billing activity, separate registration should not ordinarily be required.

-

However, where the storage facility is used regularly, forms part of recurring supply operations, or functions as a dispatch or distribution hub, it could rightfully be treated as a distinct “place of business,” requiring separate registration.

Professional Perspective

Determination of registration requirement should ideally be guided by two key aspects:

-

Intent of Use – Whether the storage is incidental to logistics or integral to supply operations.

-

Continuity of Use – Whether it represents an occasional arrangement or a recurring business function.

Businesses and professionals should therefore evaluate each warehouse or storage arrangement in light of its purpose, frequency of use, and linkage with supply activity. This proactive assessment helps avoid unnecessary disputes or notices later.

Author’s comment

The recent CBIC communication underscores the importance of correctly identifying the “place of business” under GST. While authorities may emphasize physical control and storage, the true determinant lies in the commercial intent and regularity of use.

A balanced interpretation is necessary, one that differentiates between temporary logistical handling and established supply operations, ensuring both compliance and operational practicality.

Disclaimer

This article is intended for general informational purposes only and does not constitute professional advice or an authoritative legal opinion. Readers are advised to consult their tax advisors or refer to official CBIC circulars and GST law before taking any specific action based on the above content.