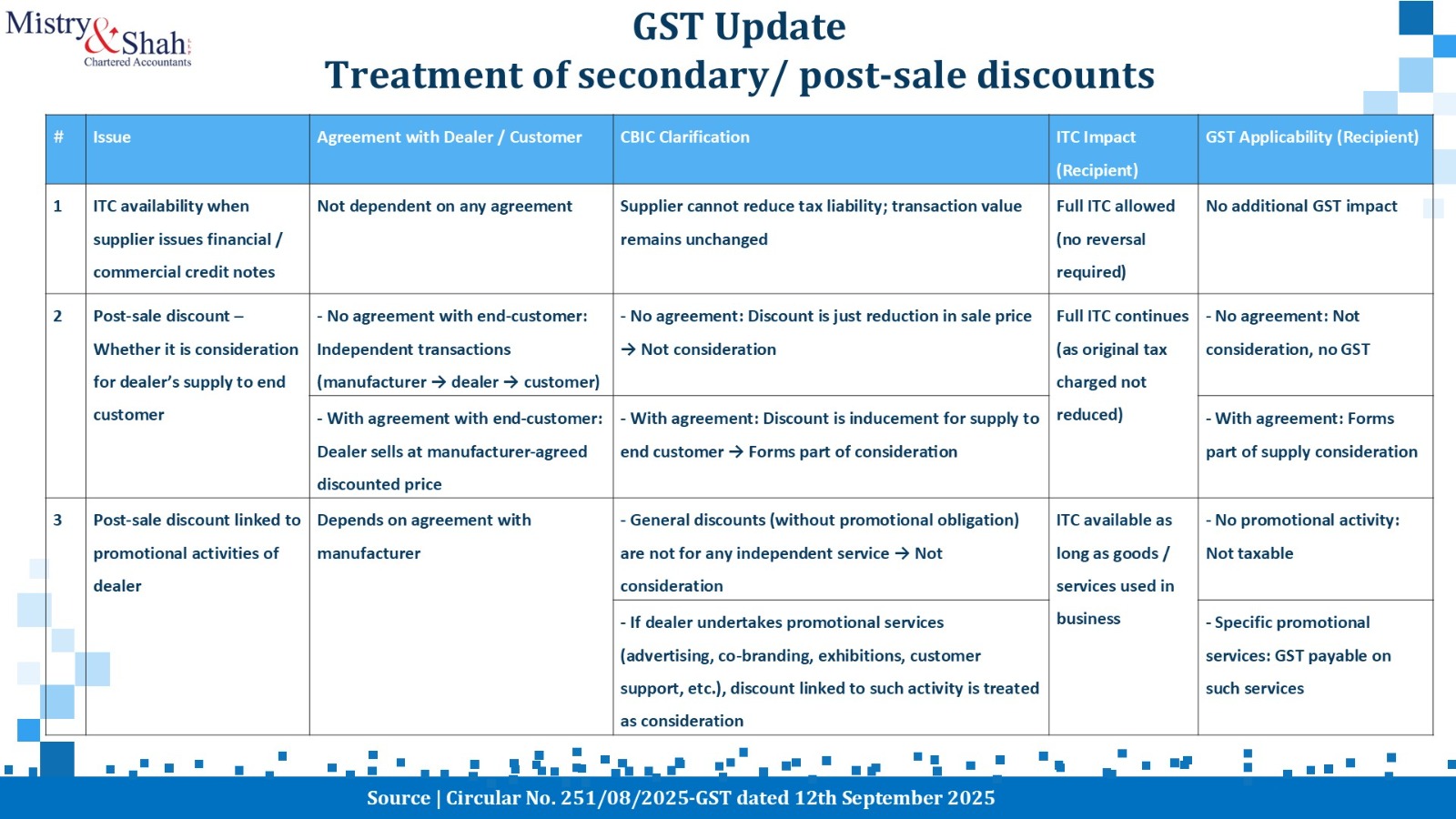

Credit notes play a vital role in the Goods and Services Tax (GST) regime, particularly in scenarios involving price adjustments, post-sale discounts, and supply corrections. While GST law envisages specific procedures for issuance and reporting of credit notes, their practical application has given rise to interpretational challenges, especially in distinguishing tax credit notes from financial or commercial credit notes, and understanding their impact on Input Tax Credit (ITC).

To bring uniformity in interpretation, the Central Board of Indirect Taxes and Customs (CBIC) issued Circular No. 251/08/2025-GST dated 12th September 2025, providing clarity on the GST treatment of secondary or post-sale discounts, and the ITC implications arising therefrom.

Understanding Credit Notes under GST

Statutory Framework: Under Section 34(1) of the CGST Act, 2017, a registered supplier is permitted to issue a credit note to the recipient when:

- The taxable value or tax charged in the original invoice exceeds the actual value or tax payable;

- Goods are returned by the recipient; or

- Goods or services are found to be deficient.

When such a tax credit note is issued, the supplier can reduce his output tax liability to the extent of tax adjustment, provided the recipient reverses corresponding ITC.

However, not all price adjustments qualify under Section 34. In commercial practice, financial or commercial credit notes are frequently issued to adjust post-sale discounts, incentives, or rebates without reducing tax liability. These are non-GST credit notes, which have no impact on tax payment or ITC availability.

Classification of Credit Notes

| Type of Credit Note | Purpose | Impact on Tax Liability | Impact on ITC (Recipient) |

| Tax Credit Note (u/s 34) | Correction in taxable value or tax | Supplier reduces tax liability | Recipient reverses proportionate ITC |

| Financial/Commercial Credit Note | Post-sale discount, incentive, or commercial adjustment | No reduction in supplier’s tax liability | No ITC reversal required (as clarified by CBIC Circular 251/08/2025) |

Key Clarifications from CBIC Circular No. 251/08/2025

Compliance and Documentation Requirements

Businesses should ensure the following documentation to defend their position:

- Distinct classification of credit notes – tax vs. commercial/financial.

- Clear agreements outlining the purpose of discounts or promotional activities.

- Defined consideration where promotional services are involved.

- Maintenance of communication trail (emails, schemes, circulars, etc.).

- Consistent disclosure in financial statements and GST returns.

Non-compliance Risk:

In absence of clear documentation, tax authorities may interpret post-sale discounts as consideration for services, leading to additional tax demands and interest exposure.

Strategic Recommendations

- Review all existing credit note mechanisms to ensure alignment with Circular 251.

- Segregate tax credit notes and commercial credit notes in ERP systems for clear audit trails.

- Document all discount schemes and promotional contracts precisely.

- Train finance and sales teams on updated GST implications.

- Reconcile ITC claims and supplier invoices regularly to prevent mismatches.

Author’s Comment:

Circular No. 251/08/2025-GST marks a significant step in resolving long-standing interpretational challenges concerning credit notes, post-sale discounts, and ITC reversals. The clarification reinforces the principle that commercial discounts do not impact ITC, while ensuring transparency in inducement-based supplies and promotional service taxation.

This move will reduce litigation, enhance certainty in trade practices, and promote uniformity in GST administration across India. However, the onus lies on taxpayers to maintain clear documentation, contractual clarity, and proper classification of credit notes to avail the intended benefits of this welcome clarification.

Disclaimer

This article is intended to provide a general understanding of the GST implications on credit notes and post-sale discounts based on CBIC Circular No. 251/08/2025-GST. It should not be construed as professional advice. For specific matters or litigation-related queries, professional consultation is recommended.